Amberoon's bank-by-bank analysis reveals a once-in-a-generation opportunity to free capital and reset strategy

Explore the full Basel III Endgame Capital Impact Dashboard at statumkpi.ai/capital-impact-dashboard.

The term Basel III Endgame has a Marvel Avengers ring to it, but this latest iteration of proposed adjustments to banking regulations is far from that cinematic universe. However, while it’s clearly aimed at boosting resilience in big banks, our own detailed analysis shows that these changes could unleash benefits for a prominent corner of the industry: community banks.

We used our signature Statum KPI's analytical engine and FFIEC Call Report data to provide granularity that few organizations have attempted: build a bottom-up, institution-level model that identifies just how these rule changes will affect all 4,236 FDIC-insured banks around the country. And the news is. . .really good and sometimes great for most institutions in this category.

We’ve compiled the results in “Basel III Endgame: A Capital Impact Analysis from a Community Bank Perspective,” a concise but comprehensive report you can download for free. We’ve also built an interactive dashboard that lets you look up your bank’s specific situation, compare it to peers, and model different scenarios. It’s free. And finally, you can enter your own questions into Ask Statum Anything, an AI-powered engine that gives you access to a world of intelligent data on your terms. It’s also free.

But to get started, here’s a taste.

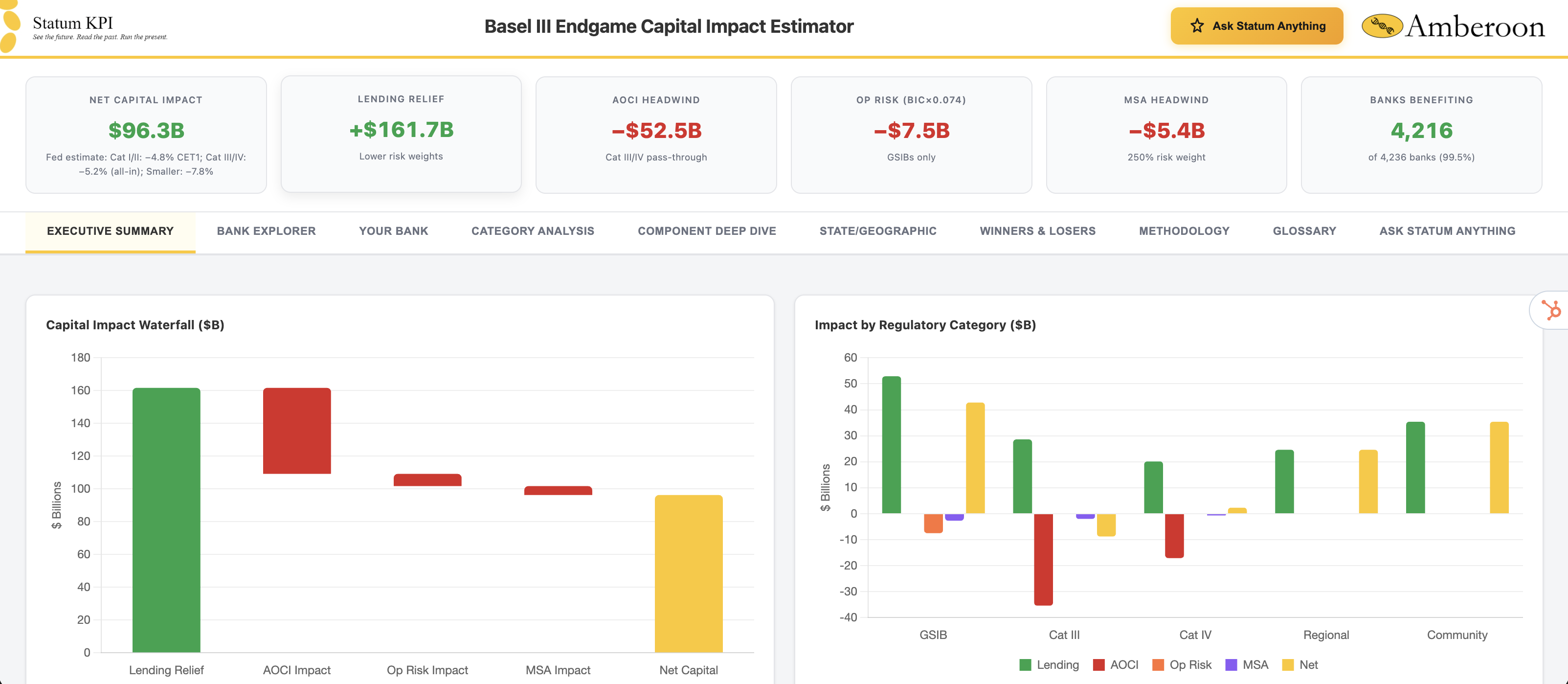

Our analysis finds that if these regulations are enacted, we’ll see $96.3 billion in net regulatory capital freed across the U.S. banking system. That is directionally consistent with (but is more specific than) the government's own Federal Reserve aggregate estimates.

But we can go further: Statum KPI allows us to pinpoint which institutions gain the most and how all this affects the bottom line.

It’s easy to understand why most of the attention around Basel III Endgame so far has zeroed in on global conglomerates with trillions in assets. It’s also true that the nine GSIB bank charters capture the largest absolute dollar benefit at $42.8 billion.

But in relative terms, the picture flips entirely.

Community banks — the 4,136 institutions under $20 billion in assets that make up the backbone of American lending — average a gain of approximately 82 basis points on their CET1 capital ratio. Regional banks average 90. This is not chump change: For a $500 million community bank, it translates to roughly $3.5 million to $5.0 million in freed capital, depending on current buffers. This is real money that can be redeployed into lending, returned to shareholders, or held as a strategic cushion.

Community and regional banks hold loan-heavy portfolios concentrated in exactly the asset classes that receive the most favorable treatment under the revised risk weights (the following are Statum KPI modeled estimates used to translate the proposal into bank-level capital effects).

- Residential mortgages drop from ~65% to a blended 38%

- Commercial real estate falls from 100% to 85% (our ERBA opt-in estimate; 95% under the Standardized Approach)

- Multifamily sees the single largest improvement, going from 100% to 70%

- Consumer loans drop from ~87.5% to 75%.

These bread-and-butter lending categories define community banking, and the new rules finally recognize that they warrant lower capital charges than the prior framework assigned.

Meanwhile, community and regional banks are expected to avoid the main standalone AOCI and operational-risk headwinds under the proposal. Most banks below $100 billion are affected primarily through revised standardized risk weights rather than those larger-bank capital overlays from the two largest headwinds in the proposal: the AOCI pass-through requirement and the operational risk capital charge. Those provisions hit Category III and Category IV banks hard, but they do not touch institutions below $100 billion in assets. The full lending relief flows straight to the bottom line for smaller banks,

The $96.3 billion net figure is the sum of four components, and each is relevant for strategic planning.

Lending risk weight relief accounts for $161.7 billion in freed capital across the system. This is the engine of the entire proposal. Lower risk weights on residential, CRE, C&I, and consumer portfolios mean less capital is required to support the same book of business. For banks with clean, well-underwritten loan portfolios, this is a big boost.

Working against that tailwind are three headwinds. The AOCI pass-through requirement creates a $52.5 billion drag, concentrated almost entirely in 21 banks — the eight Category III institutions and thirteen Category IV banks that must now flow unrealized securities losses through regulatory capital. The operational risk charge, calculated using the Business Indicator Component methodology, adds $ 7.5 billion in new capital requirements for the Category I and II banks (GSIBs). And the 250% risk weight on mortgage servicing assets creates a $5.4 billion headwind for the 39 banks with significant servicing portfolios.

For community banks, these headwinds largely do not apply. The math is simple: lending relief in, nothing out.

Not Everyone Wins

Again, 21 banks — less than half of 1% of the industry — face a net negative impact. Category III banks as a group see a net loss of $8.8 billion, driven almost entirely by AOCI. Charles Schwab Bank alone faces a $9.0 billion headwind, the single largest negative impact in the system. Truist, U.S. Bank, and several others in the $250 billion to $700 billion range are in similar straits.

This concentration of pain at the top of the size spectrum, combined with broad-based relief at the bottom, makes the revised proposal structurally favorable for community banking in a way that the original July 2023 version was not.

For the Next Board Meeting

If you’re a community bank CEO, the practical implications come down to five questions.

- How large is your bank's specific benefit? Look past the system-wide average—your number depends on your loan mix, CRE concentration, consumer portfolio, and current capital buffers. Our interactive dashboard can help.

- What will you do with the freed capital? Expanding lending capacity, improving regulatory ratios, pursuing an acquisition, increasing dividends, or investing in technology: the strategic conversation should start now, not after the final rule is issued (projected Q1 2027).

- Are you ready to speak up? You have until June 18, 2026 to submit your input, and remember—comments grounded in specific, data-driven analysis carry more weight than general advocacy. The bank-level estimates from Statum KPI can support your submission or your trade association's collective response.

- How does this change your competitive position? Capital relief is not distributed evenly. Banks with heavier concentrations in residential and multifamily lending see disproportionate benefit. If your competitors are better positioned, that is worth knowing now.

- What is your 18-month outlook? Statum KPI's predictive models can show you where your bank is headed on a standardized performance scale, accounting for these regulatory changes alongside your existing trajectory. Banks that pair regulatory awareness with forward-looking analytics are best positioned to act decisively.

Everything in this analysis is built on publicly available FFIEC Call Report data. The largest banks spend billions on exactly this kind of quantitative analysis. They model regulatory scenarios, benchmark against peers, and plan capital deployment quarters in advance.

Statum KPI was built to give community banks these very capabilities. Best of all, it’s not a watered-down version of what Wall Street uses, but rather a platform purpose-built for the realities of smaller balance sheets, relationship-driven lending, and regulatory frameworks that have historically treated all banks the same.

A note on our methodology: our $96.3 billion estimate reflects a scenario where banks elect the Expanded Risk-Based Approach (ERBA) where favorable, producing lower risk weights on CRE (85%) and consumer loans (75%). Under the NPR Standardized Approach alone, without ERBA opt-in, the net impact would be approximately $68 billion. We have disclosed every assumption, every limitation, and every data gap in our analysis. The full methodology, risk weight assumptions, and interactive tools are available at statumkpi.ai. If you think we need to modify our assumptins, we want to hear it at statum@amberoon.com.

The Basel III Endgame analysis is one example of what that looks like in practice. The full interactive dashboard, bank-specific impact estimates, and peer comparison tools are available here.

This is your time. Set the strategy, free the capital and surge forward.

For a personalized peer analysis and capital strategy consultation, contact us at statum@amberoon.com.

Explore the full Basel III Endgame Capital Impact Dashboard at statumkpi.ai/capital-impact-dashboard. We welcome your feedback on our assumptions and methodology.

Popular Posts

Last week the Federal Reserve did the one thing...

In February 2026, Anthropic ran a Claude Code...