Popular Posts

Agentic AI is a governance question wearing a...

The number 150 has a nice symmetry to it:...

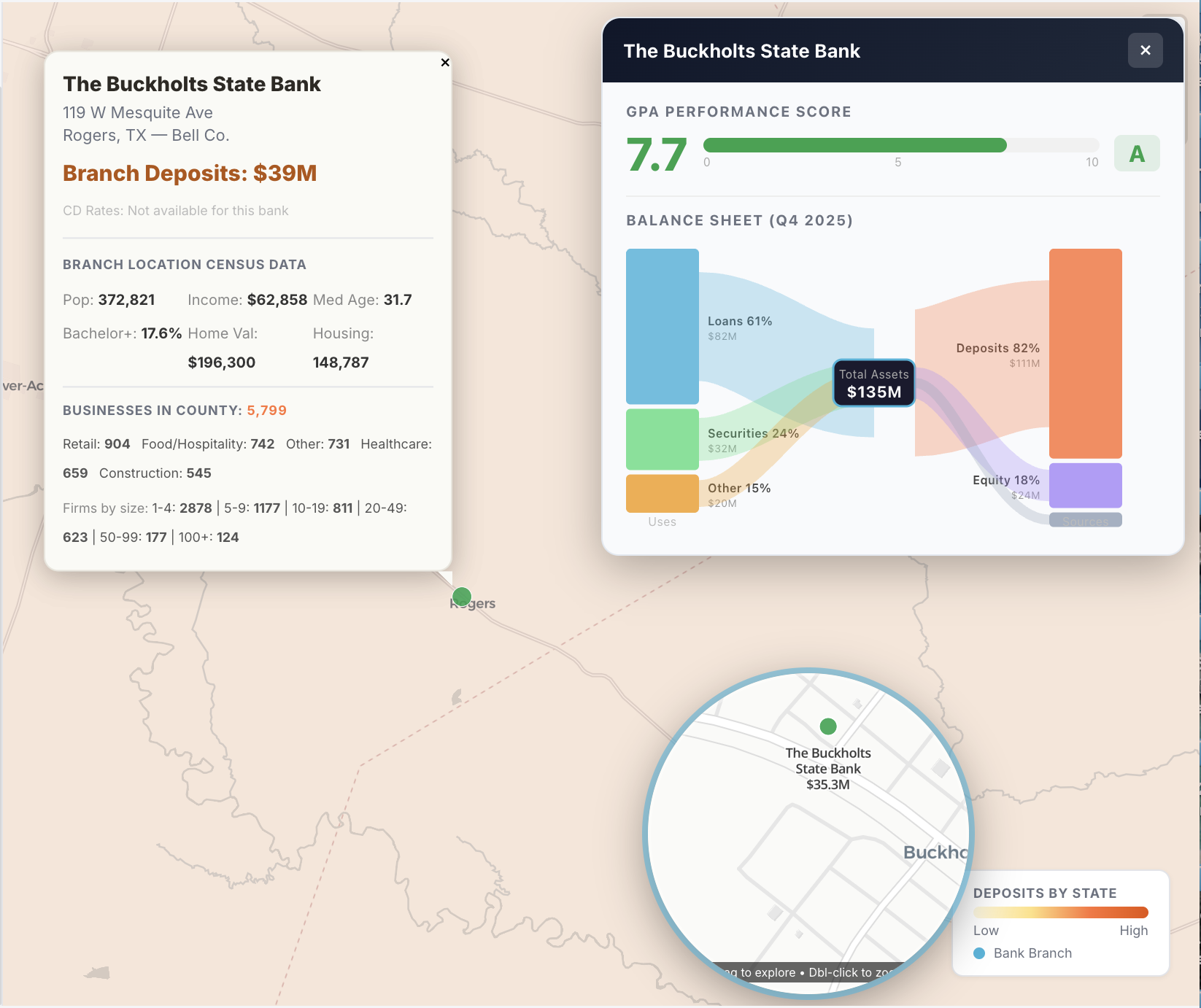

Amberoon's bank-by-bank analysis reveals a...